Foreword

Tina McKenzie,

Policy & Advocacy Chair

This latest Small Business Index (SBI) provides a measured yet encouraging indication of progress. Recovery was the third largest quarter-on-quarter rise in the history of the SBI. These figures illustrate potential to not only rebound to pre-pandemic levels, but also redefine our economy following a challenging period.

The panoramic view of progress across all sectors compared to Q4 2022 presents an interesting tableau, with strides of progress. The professional, scientific and technical sectors, for instance, saw a rise of 39.3 points, reaching a confidence score of 14.9 points, proving its robustness.

However, the wholesale and retail sector, despite a larger increase of 58.1 points, remains more negative at -25.2 points. This underlines the ongoing journey towards complete recovery.

Looking ahead, Q2 2023 presents promising prospects, with two in five small firms expecting to see an increase in their revenues. We are confident these upbeat forecasts will materialise, showcasing the steadfast drive of entrepreneurs and small businesses.

Growth aspirations, too, show a promising trend, with a slight increase from 45 per cent to 46 per cent of small businesses predicting they will grow in Q2. This aligns with a decrease in businesses expecting to downsize, sell, or close, dropping from 16 per cent to 13 per cent.

This is strong and positive, but there are still hurdles that lie ahead. Many small businesses have been impacted by increased costs, changes in finance availability, high energy and utility costs, and uncertainties surrounding exports. Employment levels also require careful scrutiny, with around one in nine firms increasing staff numbers and one in eight reducing their headcount in the last quarter. But these challenges aren’t insurmountable, and we’re steadfast in our commitment to addressing them effectively.

Despite finding the Spring Budget less supportive than expected, we will continue to press for an environment that encourages small businesses to grow, contributing to overall economic progress.

In line with this, FSB is now focusing on facilitating economic growth and fostering an environment conducive to new startups. We’re shifting our perspective from past contraction towards future expansion, aiming to reinvigorate our community with fresh initiatives and strategies, particularly emphasising start-ups and women entrepreneurs.

It’s clear that while there are challenges, there are reasons to be hopeful. The rising confidence is a promising sign, and we eagerly anticipate seeing the small business community thrive in the coming months. This is an opportunity to build stronger and better for the collective prosperity of all businesses.

Key findings

[Image text] Costs set new record

92% of small businesses report higher costs compared to a year ago

[Image text] Exporters saw a fall in volumes

40% of small exporters saw the value of their exports fall over Q1, while 37% said they stayed around the same, and 22% saw an increase

[Image text] Two in five saw revenues fall

41% of small businesses reported a decrease in their revenues over Q1, while 34% said they increased

[Image text] A third saw late payments worsen.

34% of small businesses said late payments had increased over the previous quarter

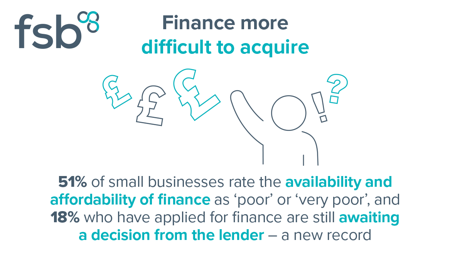

[Image text] Finance more difficult to acquire

51% of small businesses rate the availability and affordability of finance as ‘poor’ or ‘very poor’, and 18% who have applied for finance are still awaiting a decision from the lender – a new record

Executive summary

Key findings this quarter:

- The Small Business Index (SBI) increased to -2.8 in Q1 2023. This uptick follows three consecutive quarterly declines. The SBI is now at its strongest position since Q1 2022.

- All UK regions saw an improvement on the SBI in Q1, relative to Q4. Nonetheless, the SBI remained in negative territory in six of the UK’s regions and nations.

- All major industries saw an improvement in their SBI readings in Q1 2023. Most remained in negative territory, however, with construction and professional, scientific and technical businesses recording positive scores.

- The net balance of small businesses reporting revenue growth over the previous three months stood at -7.1% in Q1. This marked the fourth consecutive negative reading on this measure, reflecting the pressures on revenue from high input prices and weaker consumer demand.

- The net balance of exporting businesses reporting growth in the value of their exports stood at -17.7% in Q1. This marked the sixteenth consecutive quarter for which the net balance of exports has stood below zero. This indicates exporters are still facing unfavourable conditions.

- 91.8% of businesses reported increased costs compared to a year ago in Q1. This represents the highest net balance figure on this measure since data collection began, highlighting the widespread nature of cost pressures at present.

- Utilities were the most commonly cited source of increasing costs, selected by 62.7% of respondents. The percentage of respondents who attributed rising costs to labour saw an increase from 40.5% in Q4 2022 to 45.3% in Q1. This is likely a reflection of the combination of a relatively tight labour market and elevated inflation, with workers demanding higher wages in response to increases in the cost of living.

- A net balance of -0.8% of small businesses reported growth in employee numbers in Q1. This marks a fourth consecutive negative reading, though it was less negative than the preceding three quarters.

- For the fourth consecutive quarter, just under half of small businesses expect to grow over the coming year. However, this share was slightly higher in Q1 than in Q4 2022, at 45.9% compared to 44.7%. Weaker growth aspirations align with the general instability faced by the economy as a whole, which has experienced only marginal growth over the past quarters.

- The domestic economy is the most commonly cited barrier to growth amongst small businesses, with 61.3% of respondents selecting the category. Utility costs were the second-most selected barrier to growth amongst businesses in Q1, with 32.8% reporting this.

- The environment of higher base rates, with the Bank of England raising the base rate twice in Q1, has fed through to higher commercial rates for small businesses. The share of successful loan applicants being offered a rate of up to 4% declined starkly in Q1, reaching just 4.7%, having stood at 26.7% in Q4 2022. Accordingly, small businesses perceptions of credit availability and affordability worsened in Q1 of this year.

- Q1 brought a decline in the share of small businesses expecting to increase their investment over the coming quarter. This was the case for just 23.3% of respondents, down from 28.3% in Q4. Simultaneously, the share of small businesses expecting to cut investment over the coming quarter increased, reaching 21.2%, up from 19.0% in the fourth quarter of last year.

Click below to download the full report