Foreword

Tina McKenzie,

FSB Policy Chair

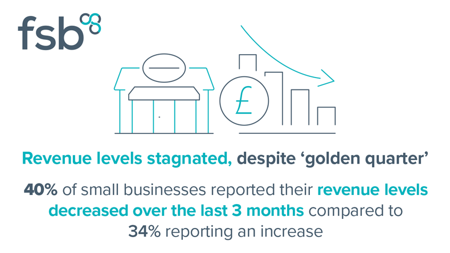

It wasn’t the end to the year that many small firms were hoping for. Small hospitality and retail businesses in particular pin their hopes on robust trading in the so-called ‘golden quarter’, which has traditionally given them enough of a cash buffer to make it through the leaner months at the start of the new year, when the festive season’s bills hit and people tend to rein in their spending.

However, the ground which had been made up in terms of small businesses’ confidence levels between the second and third quarters was lost once again in Q4. The final quarter’s headline confidence measure of -15 points was on a par with the -14.2 points recorded in Q2, after Q3’s recovery to -8 points. It’s the seventh negative reading in a row, and the worst since the same quarter in 2022, when the energy price crisis was at its height.

The sectoral results show that accommodation and food services saw by far the largest drop in confidence among the major industries, going from -31.1 points in Q3 to a highly concerning -73 points in Q4, Retail also fell, although thankfully by a lesser amount, from -22.8 to -29.8.

It’s disappointing that the tentative signs of stabilisation on some measures of small business performance in Q3 did not persist, by and large, into the final quarter. Measures including exports showed a higher net negative in Q4 than in Q3, with a modest rise in the proportion of small exporters reporting an increase in volumes (up from 24.4% in Q3 to 26.1% in Q4) more than offset by the proportion saying export volumes fell (36.9%, up from 26.9%).

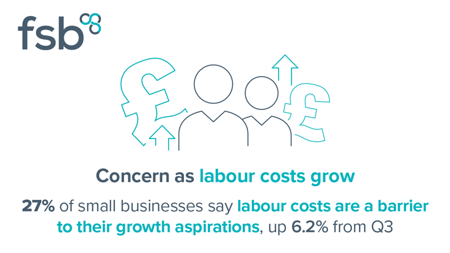

Employment levels are another sign of contraction rather than the growth we’d like to see, with one in ten small firms (10.3%) expecting to grow employee numbers over the next quarter (down from 11.7% in Q3), but with over one in nine (11.5%) expecting to reduce staffing numbers (up from 9.1% in Q3). Labour costs also saw the largest increase in citations as a potential barrier to growth, mentioned by a fifth of firms in Q3 (21.2%), but over a quarter in Q4 (27.3%). Labour costs were also the second-most cited cause of cost increases between Q4 and the same quarter in 2022, up from 42.8% in the previous survey to reach 45.7%.

The growing cost of employment underlines the need for the Government to act at the Spring Budget to reduce the burden of costs which fall on employers, through an increase in the Employment Allowance. When it was first brought in following FSB’s campaigning, it was designed to cover the National Insurance contribution costs to the employer of four full-time employees on the National Living Wage. However, the rise in the National Living Wage in April will leave it covering only three employees’ NICs costs, if its current level is not increased.

Key findings

Employment prospects fall

Labour costs grow

Revenue levels stagnated

Executive Summary

The FSB Small Business Index (SBI) decreased to -15.0 in Q4 2023 from -8.0 in Q3, indicating that SMEsexpect a faster decline in business performance than they did last quarter. This represented the SBI’s

seventh consecutive negative reading.

- These results are aligned with the downbeat picture for the wider UK economy. With GDP having contracted in Q3 and Q4, the UK economy has formally entered a recession.

- The only UK region in which small businesses expected performance to improve over the next three months in Q4 was London. Meanwhile, four regions reported a further deterioration in confidence levels, while the score for one region (the North West) entered negative territory in Q4.

- Information and communication was the only sector in which the index improved in Q4, moving into positive territory. Accommodation and food services and manufacturing were among the sectors in which performance was expected to deteriorate further over the coming three months.

- Small businesses reported falling revenues in Q4, with a net balance of -6.0% in Q4 2023. This is a slight deterioration from the -5.9% net balance in Q3 and marks the seventh consecutive negative quarterly reading. Small businesses broadly expect minimal change in their revenues over the next three months (-0.4% net balance).

- The value of exports to SMEs also fell more sharply in Q4 (net balance of -10.8%) compared to Q3 (-2.6%). This marked the nineteenth consecutive negative quarterly reading. SMEs expect a broadly flat performance over the next three months (0.8%).

- In Q4, the net balance of small businesses reporting an increase in their operating costs fell to 79.0%. This is the lowest reading for this metric since Q4 2021, reflecting the continued deceleration in inflation.

- Small businesses reported falling employee numbers in Q4 (net balance of -4.5%) and expect a further decline over the next three months (-1.2%). This is the seventh consecutive quarter that the small business employment numbers have been in negative territory. This is the first negative expectation in employment numbers over the next three months since Q4 2020.

- The share of small businesses aspiring to grow over the coming year decreased for the second consecutive quarter to 48.2% in Q4, signifying a broad reduction in confidence over the economic landscape.

- A three-year high of 15.5% of small businesses reported that they applied for credit in Q4 2023. This was up from 12.0% recorded in Q3 2023, ending three quarters of consecutive decline.

- Perceptions of credit affordability and availability continued to worsen in Q4. The credit index remains deeply in negative territory at -32.0, the joint weakest value since the series began in Q1 2022.

- The net balance of small businesses expecting to increase their investment increased to 8.2% in Q4, up from 5.7% in Q3. These changes come despite the Bank of England holding the bank rate at 5.25% since September 2023 and not being expected to cut the rate until Q2 2024.

Download the full report below