Key Statistics

Foreword

Mike Cherry,

National Chair

Martin McTague,

Vice Chair,

Policy & Advocacy

The final three months of 2021 sadly had something of a Groundhog Day feel for the small business community. Surging Covid cases, mass event cancellations, last-minute changes to trading rules and staff shortages – there was much in the challenges facing firms over this festive period that rang true for the last.

This time round though, there was also the inflation element: the proportion of small businesses saying costs are increasing is now at its highest point in seven years. Amid continued supply chain disruption, and surging wholesale gas prices, inputs and utilities are the most flagged sources of higher outgoings.

As if that wasn’t enough for business owners to get their heads around, they have, whilst trying to make ends meet, been trying to prepare for the imposition of full import checks for EU goods on 1 January 2022 and a deeply concerning moment in April when, as things stand, firms will be hit by hikes to national insurance, fresh business rates bills (now shorn of any discounts for those hardest-hit) and an increase in the National Living Wage.

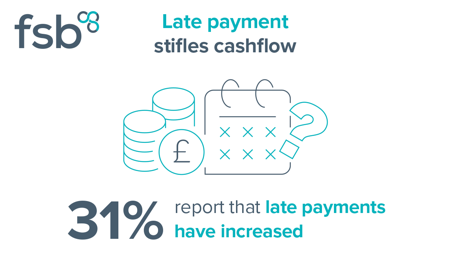

We’re hurtling towards that moment at a time when finances are already incredibly stretched. The majority of firms which participated in this quarter’s SBI report that profits are down. That’s in a climate where a million small businesses are holding emergency debt and the pandemic has exacerbated an already deeply damaging late payment crisis – more than 400,000 small firms’ futures are threatened by poor payment practice.

The upshot of these stresses and strains is that the headline UK SBI confidence measure stands at -8.5 for Q4 2022 – the first negative reading in a year, marking the fourth straight quarter on quarter drop in optimism. Worryingly, many small businesses responded to this survey before the Government announced a move to “Plan B” measures, so it is likely that confidence will have dropped further in the meantime.

As such, it needs to be new year, new policies for this Government if it’s to have any hope of reversing that trend and securing a substantial economic recovery.

Front of mind for far too many firms at this juncture is personnel. The struggle to recruit and retain the right people, which already existed pre-pandemic, is now colliding with mass self-isolation to cause a real headache for thousands. We were once promised a world-beating testing infrastructure. The Government must now deliver. Installing an education system which finally puts vocational qualifications on a par with academics alongside an immigration system that works for firms of all sizes and sectors is another must when it comes to addressing staff shortages.

Then there’s the steps policymakers can take to reduce the cost burden. The near £1 billion package of support unveiled at the back end of Q4 – encompassing fresh cash grants and Time To Pay commitments from HMRC – was a start. Crucially, that package included the return of the Covid Statutory Sick Pay Rebate for small businesses, a reinstatement we urged the Chancellor to make in our conversations with him.

That said, more will be needed to secure the futures of the many great businesses which were thriving prepandemic but are now hanging by a thread.

Given the harsh trading conditions highlighted in this report, the Government’s plan to hike the jobs tax that is national insurance looks increasingly misjudged. It should reconsider.

And with lockdowns accelerating the shift to online retail, our business rates system is looking more and more like a relic from a bygone age. The current administration should follow the Opposition’s lead in adopting our proposals to take 200,000 more small firms out of the rates system altogether, primarily in levelling-up target areas, by increasing the rateable value threshold at which firms start to pay rates to £25,000.

Where late payment is concerned, the Government promised FSB in 2019 at an event in 11 Downing Street to push ahead with reforms. However, these have not materialised. It’s time to make Audit Committees responsible for poor payment practices, and publish details of those practices in Annual Reports. This move should be central to the Department for Business’s Audit Reform package and Enterprise Strategy, both of which are due shortly. If we want to give firms the confidence to invest in net zero measures and productivity-enhancing tech, we have to bring our late poor payment culture to a definitive end.

In addition, we urgently need initiatives that can get ambitious small firms on the front foot again. Lessons should be learned from the roll-out of the SME Brexit Support Fund, with new grants made available to help those with international ambitions achieve their goals – grants which are genuinely easy to access for the smallest firms.

There’s also more to do to help small businesses contribute to the Government’s net zero aims, too. A Help To Green scheme – modelled on Help To Grow – would supercharge investment and behaviour change.

Small firms have once again shown their resilience over the past two years, tirelessly adapting and innovating, and soldiering on through yet another incredibly stressful golden quarter.

What they need now is for this Government to rediscover its pro-enterprise, reforming zeal and come forward with the policies that will empower a small business-led recovery, whilst eschewing tax hikes that will hurt communities and stifle growth.

Executive Summary

The Small Business Index (SBI) fell by 24.9 points between Q3 2021 and Q4 2021, reaching -8.5. This marks the third consecutive quarterly fall in the Index and the first negative reading since Q4 2020.

- The SBI declined in all regions except the East Midlands. This almost unanimous fall in confidence saw all regions except the East Midlands, the West Midlands and the South East entering negative territory in Q4.

- On a sectoral basis, expectations of worsening performance in the first quarter of 2022 were concentrated in manufacturing, accommodation and food services, and wholesale and retail trade. The four other sectors with sufficiently large sample sizes saw a positive, albeit falling, SBI reading in Q4. The largest quarterly falls among sectoral SBI readings were seen in accommodation and food services, which fell by 35.4 points to stand at -33.0, and information and communication, which saw a reduction of 35.1 points to stand at 11.4.

- A net balance of 4.8% of responding small businesses reported a fall in gross profits in Q4. Furthermore, looking ahead, more small businesses expected their profitability to reduce than increase in Q1 2022, although this saw a smaller net balance reading of -3.3% compared to the actual experiences in Q4.

- Exporters fared worse than they had expected in Q4. The net balance of exporting businesses reporting growth in the value of their exports amounted to -12.3% in Q4, up from -20.0% in Q3. However, at the end of Q3, a net balance of -4.6% of exporters had anticipated export growth in Q4, such that activity in the latest quarter was worse than expected.

- Rising costs of production continued to represent an area of concern for businesses in Q4. Over a fifth (20.3%) of responding firms noted experiencing a significant increase in operating costs (a rise of over 10%) in the final quarter, compared to the same period one year previously, with over three-quarters (78.2%) experiencing an increase of any size. The Q4 net balance reading represents the highest since Q4 2011, the last period of comparable cost pressure.

- Being selected by 48.7% of firms, inputs remained the most common source of cost changes for the fourth consecutive quarter. As was the case in Q3, this was followed by fuel costs (45.6% of firms) and utilities costs (44.8%), whilst rising labour costs also continued to bite (38.0%). These areas of influence on costs reflect the broader pressures caused by supply chain disruptions and soaring energy costs in the second half of 2021.

- The number of survey respondents reporting an increase to the size of their workforce in Q4 outweighed the number reporting a decrease. With a net balance of 3.3% experiencing growth, up from -0.2% in Q3, workforce numbers returned to growth in the final quarter. This favourable picture for employment in the final quarter came despite the termination of the Coronavirus Job Retention Scheme (CJRS) at the end of September. Even greater optimism was seen with regard to business employment in Q1 2022, with a net balance of 9.8% of firms expecting growth, despite concerns over the emergence of the Omicron COVID-19 variant.

- The share of businesses aspiring to grow increased by 1.0 percentage points in Q4 to reach 54.1%. The domestic economy remains the most common barrier to growth, being selected by 56.7% of responding businesses. Q4 saw the first quarterly rise in the share of firms citing this option since Q2 2020, a potential reflection of increased uncertainty in light of the Omicron wave. Among the next key barriers, access to appropriately skilled staff became less significant in Q4 compared to other factors, whilst consumer demand became of greater concern.

- Following the previous record low in Q3, the proportion of businesses applying for credit fell further to 9.5% in Q4. This represents the lowest level for this measure since SBI data collection began. The credit availability and affordability indices worsened to levels not seen since Q1 2020, with readings of -10.8 and -11.4, respectively. Affordability is likely to worsen further in Q1, following the Bank of England’s December rate hike.

Click below to read the full report