Introduction

The past two years have thrown up all kinds of economic quirks and firsts, as markets shift in response to Covid-linked disruption and new ways of working. To the growing list of unexpected stats and forecasts, the Small Business Index can now make its own contribution: confidence among firms dropping for two straight quarters as trading restrictions lift.

Counterintuitively, the headline SBI confidence measure has fallen more than two points this quarter compared to last to stand at +16.4, and is now down more than ten points on Q1 of this year. A positive reading of any kind, after last year’s rock-bottom index scores, is to be welcomed.

But that statement comes with significant caveats.

The SBI is a forward-looking confidence measure, with respondents setting out how they expect their business to perform over the coming three months compared to the previous three. At the time of writing, Q4 is set to be unique – the first round of largely unencumbered festive season spending for what will, for many, feel like a very long time indeed. As such, we should be seeing a small business community that’s bullish, high-spirited and raring to make up for lost time after a prolonged period of on-again, off-again restrictions.

In reality, whilst a significant proportion are forecasting an improvement in performance, the majority are not, and close to one in three expect a deterioration. The main clues as to what’s driving this drop-off in optimism reside in responses to question nine of the SBI. This is where we ask respondents to list their three biggest perceived barriers to business growth over the coming year.

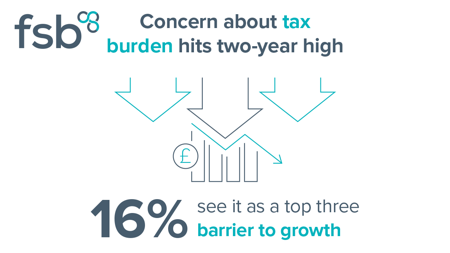

The proportions flagging the ‘domestic economy’ and ‘consumer demand’ fell dramatically this quarter, reflecting a measure of relief as restrictions ease. By contrast, the shares stating that the ‘tax burden’, ‘fuel costs’, ‘labour costs’, ‘input costs’, and access to ‘appropriately skilled staff’ are holding them back have all soared over the last twelve months, in many cases to levels not seen in years.

This was the quarter in which the Government declared that National Insurance contributions – an indiscriminate charge on all employers, employees and sole traders – will be hiked by 1.25 percentage points in the spring. Directors too, who were excluded from the Government’s income support initiatives, will be hit by a dividend tax increase. We estimate that the move will mean at least 50,000 more people becoming unemployed once it takes effect, and we also asked members how they would respond to the change as part of this SBI.

Among employers – when coupled with a 6.6 per cent increase in the National Living Wage – one in three say they would be forced to increase prices, further adding to existing inflationary pressure. One in four say they would absorb the additional cost personally, and the same proportion say they would recruit less and/ or reduce existing worker hours. So, in short, unless the Government does more to help small firms with the spiralling costs of utilities, employment and fuel, it’s risking a real flashpoint in April.

And whilst we’ve conducted and published a thorough and transparent risk assessment of the NICs hike, policymakers are yet to. To enact such a significant change without analysis of likely outcomes is reckless at best. It should also be mentioned that shipping costs too are going through the roof, adding to the myriad pressures faced by firms that trade globally. This SBI finds that one in five exporters have either permanently or temporarily halted overseas sales. Fresh admin resulting from a new EU-UK trade agreement, supply chain disruption – delays in moving products, and even losing them in transit altogether, are now, sadly, par for the course – as well as the increase in the cash needed to ensure products reach clients have all taken their toll.

Fundamentally, the Government’s optimistic talk of a “low-tax, high-productivity economy” is not currently matched by sentiment on the ground. There is still time to act to deliver this commendable vision, and act policymakers will need to if we’re to avoid a third straight quarterly decline in small business confidence.

With all eyes on GDP figures as we seek to recover from one of the most severe economic shocks in modern history, this is a moment when we need optimism and confidence among the small businesses that can make all the difference to be the stuff of lived realities, not just speeches.

Mike Cherry,

National Chair.

Martin McTague,

Vice Chair,

Policy & Advocacy

Key findings

Executive Summary

The Small Business Index (SBI) slipped by 2.2 points between Q2 2021 and Q3 2021, reaching 16.4. This marks the second consecutive quarterly fall in the Index, following the near-term high of 27.3 in Q1.

The Small Business Index witnessed a decline in nearly all regions. Only London and the combined region of the North East and Yorkshire and the Humber saw their SBI readings increase compared to Q2. Nevertheless, all regions but the East of England and the East Midlands exhibited positive readings in Q3, suggesting that sentiment of improved performance is well-spread geographically.

Most major sectors expect improved performance in the final quarter of the year. Of the sectors with sufficiently large sample sizes, only wholesale and retail exhibited a negative SBI reading in Q3, standing at -10.5. This pessimism can be explained by the recent experience of countercyclical retail activity, as well as fears that supply shortages could disrupt trading in the busy festive period.

The net balance of small businesses reporting an increase in operating costs increased further in Q2, reaching a more than two-year high of 69.5%. This reflects the near-global phenomenon of rising producer prices.

Inputs were the main driver of changing business costs in Q3. This category was cited by 47.0% of small businesses when considering sources of cost pressure. Fuel and utilities represented the next most commonly cited categories, being selected by 37.3% and 36.5%, respectively, reflecting rising prices in oil and gas markets.

The net balance of small businesses expecting their employment levels to increase in Q4 stands at 11.5%, although employers report negative growth in employment in the last quarter – contrary to previous expectations. There is considerable regional variation in employment expectations, with a net balance of 19.8% of businesses in London expecting employment growth in Q4, compared to just 2.8% in the East Midlands.

The share of businesses aspiring to grow over the next twelve months decreased slightly, reaching 53.1%. Growth aspirations are most prevalent amongst businesses in the information and communication sector, with greater adoption of technology in the wake of the pandemic being one likely factor behind such positivity.

The domestic economy remains the most commonly cited potential barrier to growth, amongst those with aspirations to grow. Though this was the case for 54.6% of respondents, this was the fifth consecutive quarterly fall in the proportion of businesses citing this option.

The proportion of small businesses applying for credit reached its lowest level since data collection for the SBI began. Just 10.4% of businesses applied for credit in Q3. This could reflect the fact that businesses’ operations are beginning to normalise, thus reducing the need for short-term cash flow support, as well as some lingering uncertainty reducing the incentive to invest.

Click below to download the full report