Foreword

Martin McTague,

National Chair

Tina McKenzie,

Policy & Advocacy Chair

The second quarter of 2022 will not be remembered with much fondness by the majority of small business owners. After a surprisingly upbeat start to the year, with the headline Small Business Index reading back in positive territory in Q1 following an Omicroninduced return to the negative zone at the end of Q4, the Q2 2022 temperature check for small firms is once more deeply negative. Indeed the change from +15.3 in Q1 to -24.7 in Q2 is the second-largest fall in the Index’s history, and is surpassed only by the quarterly fall registered in Q1 2020, when the pandemic first hit the UK.

With the economic impact of the Covid-19 pandemic less apparent in Q2 than during the previous two years, the main culprit for this precipitous drop in small business confidence levels must be inflation, which during the quarter in question reached a 40-year high.

Every conversation FSB has had with our members over the past few months has touched on two issues - spiralling costs, and a stark shortage of labour. Cost increases are now affecting everything from the price of petrol to cooking oil to timber to orange juice to laundry detergent, and much more besides. Inflation is the overriding economic concern among FSB’s membership, with the series-high reading of 89.0% of firms reporting higher costs than a year ago a stark illustration of the toll it is taking. The cost of doing business crisis, which we raise frequently with politicians and the media, is in turn adding to the cost of living crisis affecting households, as businesses have no other choice than to pass on higher costs, creating a vicious circle. The cost of doing business crisis has exacerbated a crunch on small businesses being able to recruit talent, which may mean this autumn businesses having to close their operations on days without staff cover, and to save on exponential energy bills.

The suppression of small businesses’ ability to grow and invest, by making it impossible for all too many of them to think about anything beyond survival, is a sign that the UK’s long-running ‘productivity puzzle’ looks set to stay in place for some time yet. Some say certainty is what small businesses crave; however, a certainty of rocketing costs and prices into the medium term will do the opposite, making many small businesses simply unviable. It’s hardly surprising that they are battening down the hatches, focusing on the essentials, and looking to cut costs wherever they can, rather than seeking funding to invest in new technology, premises, or processes.

Growth is firmly off the menu for the majority of small businesses, with 38.7% planning to stay the same size, and 14.7% - one in seven – expecting to downsize or even close their business over the next 12 months. The success of small firms’ credit applications remained well below the pre-pandemic trend, at 44.9%, while the number of firms reporting they had even applied for finance in the first place was 11.5%, up from the record low of 9.1% in Q1 2022. The credit on offer has also ticked up in price, a predictable consequence of the rise in the Bank of England base rate seen over the quarter, but an additional pressure on budgets nonetheless, and one likely to get worse in the coming quarter, given the 50 basis point rise decided in August.

Likewise, the first fall in employee numbers since Q1 2021 was recorded, falling far short of relatively buoyant hiring intentions in last quarter’s survey, and showing the speed with which inflation pressures have overtaken many firms’ plans. Access to skilled staff also ticked upward as a cited barrier to growth, up to 33.9% in Q2 from 31.3% in Q1, with the domestic economy however far and away the most-cited barrier to growth, at 65.1%, up from 58.6% in the previous quarter.

It is beyond clear that the Government needs to act, to help businesses facing acute pressures. The next Prime Minister must affirm their commitment to small businesses, self-employed people, and entrepreneurialism, and take swift action on urgent sources of pain which threaten the survival of countless firms. A reversal of the National Insurance hike, which came into effect during Q2, cuts to VAT and fuel duty, a fresh look at business rates, and help for small businesses with soaring energy bills must all be on the agenda. The economic devastation that inaction would cause must spur decisive intervention, before it is too late for countless small businesses.

Key statistics

[Image text] Costs reach a new high. 89% of small businesses report higher costs compared to a year ago.

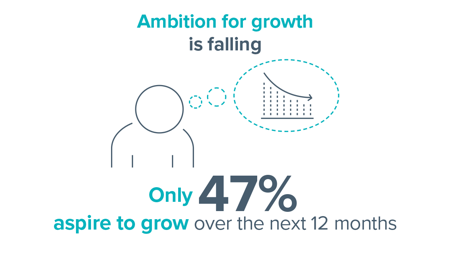

[Image text] Ambition for growth is falling. Only 47% aspire to grow over the next 12 months.

[Image text] Small businesses are struggling to access finance. Just 45% of financial applications were successful in Q2

Key findings

The Small Business Index (SBI) fell to -24.7 in Q2 2022, a drop of 40.0 points. This marks the second largest fall in the history of the Index, only being outweighed by the drop of 121.8 points in Q1 2020, when the Covid-19 pandemic first hit the UK.

The SBI fell across all regions in Q2 2022 compared to Q1. Furthermore, all regions showed a negative reading, ranging from -43.4 for the East Midlands to -10.3 for the East of England. This highlights the widespread nature of the pressures facing the economy, which are feeding into business performance regardless of geography.

The SBI deteriorated across all major industries in Q2 2022. In addition, SBI readings for all industries are now in negative territory. This is in stark comparison to Q1, when only two industries, wholesale and retail trade and manufacturing, saw a sub-zero score.

The net balance of small businesses reporting revenue growth over the previous three months stood at -6.0% in Q2 2022. A negative reading was last witnessed in Q1 2021, when businesses’ revenue streams were significantly curtailed by the third national lockdown and the accompanying slump in economic activity.

The net balance of small businesses reporting an increase in operating costs increased for the fifth consecutive quarter in Q2, reaching a new series high of 85.9%. This illustrates the extent to which businesses have experienced cost pressures in recent months.

Increased costs are being driven by fuel, utilities, and broader inputs amidst shortages and market volatility. There was also a stark increase in the share of firms reporting the exchange rate as a source of increased costs, reflecting the weakening of sterling in recent months.

The net balance of small businesses reporting growth in employee numbers stood at -3.6% in Q2, down from 2.9% in Q1. This marked the first negative reading on this metric in over a year.

A net balance of 31.9% of small businesses expect to grow over the coming year. This is a considerable deterioration from Q1, when the net balance stood at 39.1%, highlighting the dampened economic outlook that has emerged in recent months. The domestic economy remains the most commonly cited barrier to growth amongst respondents.

The rate of credit applications ticked up in Q2, to 11.5% of businesses in Q2. This was up from just 9.1% in Q1 and likely reflects businesses’ attempts to cover mounting cost pressures.

After investment intentions had already fallen in Q1, the deterioration continued in Q2 2022. 22.7% of businesses planned to increase their capital investments over the coming quarter. This is down from 23.4% in Q1 and the lowest share since Q1 2020. Widespread uncertainty and increased borrowing costs represent two key factors behind this slump in investment intentions.