Foreword

The second quarter of 2021 had its ups and downs for small businesses, with good news about falling Covid hospitalisations countered by a postponement of full reopening in England, without an accompanying extension to business relief measures, and Covid app pings hampering access to staff. Small firms in Wales, Scotland and Northern Ireland also faced uncertainty on the timings of restrictions easing.

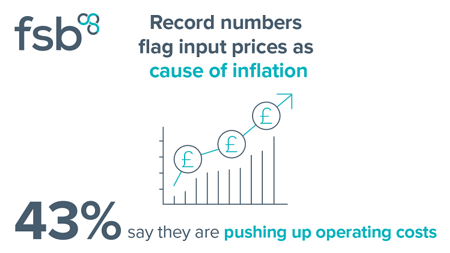

While small business confidence growth has slowed down since the last quarter, it has held up to a considerable degree, down to the greater certainty provided by the Government’s roadmap out of lockdown. Respondents are more bullish about their profit expectations than they were six months ago, and indeed this time in 2020. But it isn’t plain sailing, with the proportion saying that the cost of running their business is higher than it was last year jumping sharply. Rising input costs are a particular area of concern, with many small businesses acutely exposed to fluctuations which eat into their already-eroded profit margins. This increase plays into the prospects of higher inflation, which could hamper a forecast recovery.

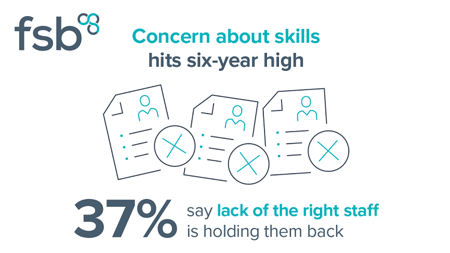

More small businesses are raising a lack of appropriately skilled staff as a barrier to growth than in previous quarters. Ensuring that small businesses can access the right level of skills, especially in high-growth sectors and industries essential to the functioning of the economy, should be a key priority for the Government. New initiatives around apprenticeships, traineeships, T-level placements and Kickstart should be expanded to have a greater impact. The quarter covered in this report saw businesses still benefiting from some pandemic-related support schemes, with rises in employers’ contributions for furloughed staff and deferred VAT repayments kicking

in only at the start of Q3.

The extension of the moratorium on commercial evictions for businesses hit by the pandemic until March 2022, and the announcement that the restrictions on issuing statutory demands will remain in place until the end of September, were twin pieces of good news for many small businesses. Easy measures for the Government to sign off, of course, as they do not require contributions from the public purse.

Thousands of companies which took out state-backed loans started making their first repayments in May. Almost two in five SBI respondents who have some form of debt view it as unmanageable, while small businesses’ view of the affordability of new credit has deteriorated since the last survey. We’re urging Bounce Back Loan providers to make all relevant customers aware of their Pay As You Grow Options and encouraging the Government to look again at our emergency debt for employee equity model.

One perennial concern is the late payment crisis, which has worsened through the epidemic. The damage poor payment practices cause to small businesses is both enormous and unnecessary. It is completely unjustifiable for customers to delay payments, effectively using small suppliers as free credit lines.

FSB is calling for companies’ payment practices to be made more visible at board level, with accountability processes in place to ensure that the issue is taken seriously at the very top of big corporates. We look forward to working with the new Small Business Commissioner on this front.

Looking ahead, there are many reasons to be optimistic. If hospitality, accommodation and independent retail businesses are able to remain open in the face of fears about staff being pinged, the ‘staycation summer’ should spur recovery in many areas, especially coastal towns where a good summer is vital for local economies.

There are possible clouds on the horizon, from the threat of a new strain of Covid taking hold, to issues around Covid passports, to the levels of debt which many small businesses were forced to take on in

order to survive, and which may now hamper their efforts to rebuild.

As we work towards recovery, we hope that the UK Government will honour its manifesto pledge to be a pro-small business administration. We hope too that it realises the centrality of small businesses and the self-employed to its levelling-up agenda: whether it’s streamlining and improving business support to drive productivity, or creating new jobs in local communities, ministers will need to think small first to succeed.

While the resilience and adaptability of small firms are there for all to see, the Government still has a critical role to play in supporting them, to the overall benefit of our economy and future prosperity.

Key findings

The Small Business Index (SBI) slipped by 8.7 points between Q1 2021 and Q2 2021, reaching 18.6. This marks the first time the Index has exhibited positive values in consecutive quarters since Q2 2018.

- With the exception of London, unanimous positivity on the SBI was observed across all regions. The East Midlands was the region with the highest rate of confidence, as had also been the case on the previous round of the survey.

- Most industries expect improved performance in Q3. With the exception of wholesale and retail, all of the industries with sufficiently large sample size exhibited positive readings on the SBI looking ahead to Q3. The figures for wholesale and retail was neutral, at 0.0, suggesting that such businesses expect performance to continue at its current level.

- More small businesses saw profitability decline than improve in Q2. Nevertheless, businesses are much more optimistic surrounding profitability, with a net balance of 8.6% of respondents expecting an improvement in Q3. This represents the highest reading on this metric since Q4 2015.

- Exporters fared worse than they had expected in Q2. When questioned at the end of Q1, a net balance of -9.8% of exporters had anticipated export growth in Q2, indicating a difficult outlook for trade. Q2’s actual data yields an even more negative net balance figure of -19.8%.

- The net balance of small businesses reporting an increase in operating costs increased starkly in Q2, reaching 53.2%. This marks a record quarterly uptick of 29.9 percentage points on this metric. The reopening of the economy has been a clear driver of year-on-year increases in costs, with the renewed activity stoking inflationary pressure in a number of categories. Variable costs, such as inputs and labour, were the main drivers of this increase.

- The number of businesses reporting an increase to the size of their workforce in Q2 outweighed the number reporting a decrease. A net balance of 2.2% reported workforce growth. Looking ahead, small businesses are even more optimistic about the size of their workforce, with 14.0% anticipating further growth in Q3.

- The share of businesses aspiring to grow increased by 1.7 percentage points in Q2, reaching 54.4%. The domestic economy remains the most common concern for businesses when considering barriers to growth, though the extent to which this is the case is subsiding. Appropriately skilled staff is also a commonly cited barrier, aligning with recent reports of labour shortages.

- The credit availability and affordability indices fell in Q2, reaching their lowest values since Q1 2020. Meanwhile, the proportion of small businesses seeking credit subsided further in Q2, reaching pre-pandemic levels.

Download the full report