Foreword

The UK Government has embarked upon a Tax Administration Framework Review with the aim ‘to design a trusted, modern tax administration system that is simpler, easier to navigate and more responsive to taxpayers’ needs. In order to inform its response to HMRC’s call for evidence, FSB has commissioned a comprehensive, in-depth survey of members’ experiences of the tax system. The survey clearly shows that the current tax system, with its plethora of taxes, reliefs, and thresholds, is too complex, expensive in time and money to comply with, a substantial barrier to growth, and inherently unfair for SMEs. Small businesses do not have the dedicated tax teams and specialist knowledge available to large corporates and consequently they miss out on many reliefs. SMEs face a disproportionate compliance burden relative to turnover.

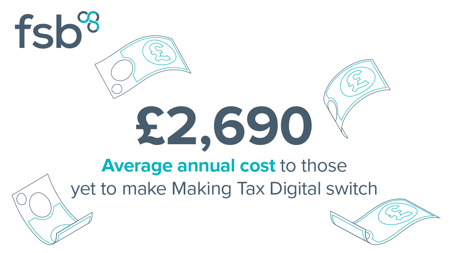

FSB welcomes the move to reform the tax administration system. The current system is based on the Taxes Management Act 1970 with half a century of subsequent incremental adjustments. It is not fit for purpose in a digital age. The introduction of Making Tax Digital (MTD) was supposed to alleviate many of the issues arising from the hyper-complexity of the tax system, easing tax compliance, increasing efficiency, and aiding cashflow planning for businesses. Yet, just over two years since its initial introduction, small businesses are complaining that MTD has done little to smooth the tax administrative process but has significantly increased their costs of compliance.

In order to be trusted, any new system must not only be fair in design; it must also be fair in operation. With a large majority of taxpayers’ complaints reportedly upheld, especially those concerning automatic, computer-generated charges, the burden of checking liabilities wastes time and resources that could be used to grow businesses. The tax system needs to be fully transparent. Small businesses are now required to use approved software to report to HMRC. For many, the software subscriptions have added significantly to their compliance costs. There is genuine concern that these software subscription costs will continue to

increase as MTD spreads across the different taxes. MTD is a major reform step that will require continual adjustments. We urge HMRC to ensure that its MTD framework is developed to alert small businesses to available reliefs.

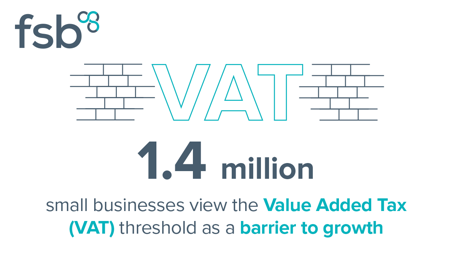

A fundamental principle of good taxation is that it should be neutral in its impact on economic decisions, except where deliberately designed for a public-good end, as with the sugar tax. The current system erects significant barriers to growth. Most notably, the current VAT threshold is a major constraint on business growth with many businesses deliberately restricting their turnover to below £85,000. The costs associated with employing people also hinder business expansion.

FSB acknowledges that the Government needs to restore public finances following the sharp rise in public sector debt resulting from the pandemic. We support measures that would reduce the tax gap – all taxpayers should pay the right amount due and MTD should help with this. However, we note that the recent introduction of a Health and Social Welfare Levy adds to the complexity of the tax system and is a tax on jobs, which will impede business growth.

The best way for the Government to bring down the budget deficit, is to encourage economic growth, thereby raising tax revenue. The recommendations put forward in this report are designed to help ensure that the tax system is supportive, not destructive, of growth in the vital small business sector.

Key Findings

Our recommendations

The basic VAT taxable turnover threshold should be raised from £85,000 to £100,000 to encourage suppressed economic activity. VAT payments should also be smoothed, as suggested by the Office of Tax Simplification (OTS), to minimise the immediate VAT liability businesses receive once passing the threshold. HMRC should also retain its central focus on ensuring that Making Tax Digital for VAT alleviates the administrative burden of paying liabilities.The VAT threshold at its current level acts as an artificial barrier to growth for 24 per cent of small businesses. Small businesses have explained that they have taken measures to reduce their economic activity to ensure that they do not cross this threshold and become liable to pay the tax. This tax threshold is therefore supressing genuine economic development in the economy. A higher threshold level could unlock this pent-up activity and bolster the economy, especially in light of the COVID economic crisis. Likewise, a stepped rate increase in the form of a smoothing mechanism, as suggested by the OTS, also ensures that businesses are not faced with a significant liability once the single threshold is reached. By raising the top threshold to £100,000 and including a smoothing mechanism, HMRC will encourage growth while also raising revenues.

Given the significant burden of tax compliance for small businesses, the Government should not exclude tax administration costs from regulatory oversight, and should ensure that any changes in regulation policy do not add to the burden already faced. Taxation is the second most burdensome form of regulation that small businesses have to comply with. However, the Regulatory Policy Committee (RPC) excludes any impact assessments that relate to tax or spending decisions while still stating that its role is to ensure the Government has minimised the regulatory burdens on small and micro businesses. This is a significant inconsistency. We urge the Government to expand the scope of the RPC to include taxation, such that the large regulatory burdens of and changes to taxation are regularly assessed for their impacts in line with other regulatory changes. The exclusion of the regulatory burden of taxation undermines the whole process of reducing the regulatory burden small businesses face.

The Government should introduce a system whereby the self-employed can smooth their income tax liabilities over a three-year rolling average through the availability of tax credits. Three quarters of small businesses struggle to accurately forecast their earnings each year, and state that their financial security fluctuates. The Government could alleviate many concerns around income through introducing a three-year rolling average taxable income scheme for the self-employed. This would limit small businesses’ exposure to shocks to their income, as they would be able to offset losses on the previous two year’s gains. Looking backwards, where a year’s income exceeds the three-year average, that effective overpayment could be considered a tax credit towards liabilities in years where income is below average, thus smoothing overall liabilities.

The Government should expand reliefs on investment to ensure that businesses are no longer deterred from investing more in the economy. Small businesses would be more likely to engage in investment and R&D if they knew they could write off losses at a similar rate at which gains are taxed, producing a more symmetrical and equal system. The ability to write off losses means that investments that do not yield expected results may not be as devastating to a business as they may otherwise be. Overall, more investment in the economy is the Government’s ambition and this would significantly encourage small businesses.

The Government should reform the Super Deductions investment incentive. There is insufficient clarity available to small businesses as to the scope of the super deduction, particularly it’s applicability to intangible investments. A tax incentive that is too opaque will not work as intended if it is not readily understood by the population it is meant to influence.

Moreover, only four per cent of small businesses rated it in their top three incentives, which shows it is of very limited use to small businesses. This is despite the fact that this incentive was projected in Budget 2021 to cost the exchequer over £12bn a year. Given the recent increases that have been announced to National Insurance Contributions – a tax on jobs which will hit small businesses hard – we believe it would have been more appropriate to reduce the cost of the super-deduction.

The Government should promote greater awareness of the tax reliefs available to small businesses, both externally and through Making Tax Digital software. Small businesses have limited awareness of the available tax reliefs they may be eligible for, which means they pay their fair share of taxes, but don’t get their fair share of reliefs. Small businesses are on average only aware of five reliefs – a very small number considering the wide variety available. Fixing the gap in knowledge around reliefs would go a long way towards restoring more faith that the tax system is fair towards small businesses; they pay their liabilities and thus should receive their fair share of reliefs. The Government ought to do more to publicise available reliefs for small businesses such that their use is maximised, addressing the fairness issue within the tax system. We urge the Government to create a system within the Making Tax Digital software that utilises the information provided by businesses to create nudges around potential reliefs they could apply for. Importantly, this should be a free feature of all Making Tax Digital software and not a paid-for add-on.

The Government should commit to ensuring that the software providers of MTD do not increase prices in a rent-seeking manner. Making Tax Digital has already created a significant cost burden to small businesses that have adopted it. There is genuine worry amongst small businesses that this cost will only increase as they become more dependent on Making Tax Digital-compatible software for returns. We urge the Government to commit to ensuring a competitive market exists within MTD-software such that rent-seeking behaviour is minimised, and prices remain competitive.

The Government must provide a free online tool for Making Tax Digital to ensure that small businesses have the choice not to be burdened by additional costs to file their taxes. The cost burden of tax filing is already significant to small businesses, and Making Tax Digital has not eased this situation. For the complete rollout, a free online tool should be made available so that the smallest of businesses do not need to acquire costly subscriptions for tax administration services they may not fully utilise.

HMRC must work with software providers to ensure that the Making Tax Digital software does streamline, simplify, and create greater efficiencies in tax compliance, and ensure that Making Tax Digital actually provides additional value. Making Tax Digital is viewed by small businesses as relatively burdensome – 71 per cent agree it has increased the cost of tax compliance through new software, subscriptions, and time spent learning the new processes. However, MTD has done little to address the fundamental issues in the tax system; few agree that complexity has decreased and that cashflow management is easier. We urge the Government to continue to work towards these goals, and to address the issues of complexity and cashflow management through Making Tax Digital while keeping a small business focus. We would also like to see the OTS become more directly involved in the process, ensuring that the final MTD product does indeed simplify the complexities of the tax system.

The Government should increase the Employment Allowance to £5,000 for eligible small businesses to alleviate some of the job losses from the planned National Insurance contributions increase. Employer National Insurance contributions act as a tax on jobs. The recently announced increase of 1.25 percentage points is going to have a detrimental effect on jobs throughout the UK and will disproportionately affect small businesses that will now face a greater employment cost bill. Over one million small businesses used the Employment Allowance in the last financial year, the vast majority of them being micro employers.

The Government is funding its own departments at a cost of £1.8 billion so as to not reduce their spending power in light of the NICs increase. This should be extended to small businesses, alleviating employment cost pressures, aiding their post-pandemic recovery, and sustaining employment throughout the UK.